POSTED ON: DECEMBER, 2019

AUTHOR: BRUCE LUEBKE, COMMUNICATIONS AND CONTENT COORDINATOR

AUTHOR: BRUCE LUEBKE, COMMUNICATIONS AND CONTENT COORDINATOR

Buying a home will likely be one of the most significant purchases of your life, and you’ll usually need a loan to make it happen.

When the time comes, it’s essential to do your research so that your mortgage is the right fit for you.

Mortgages can be a little intimidating and confusing, so here are some of the basics to help you understand how they work.

Financial institutions have mortgage products with an advertised Annual Percentage Rate (APR) or interest rate. Getting a low APR is an excellent start to an affordable mortgage, but it doesn’t tell the whole story. There is a wide range of additional costs to consider, including insurance, taxes, admin fees, penalties, etc.

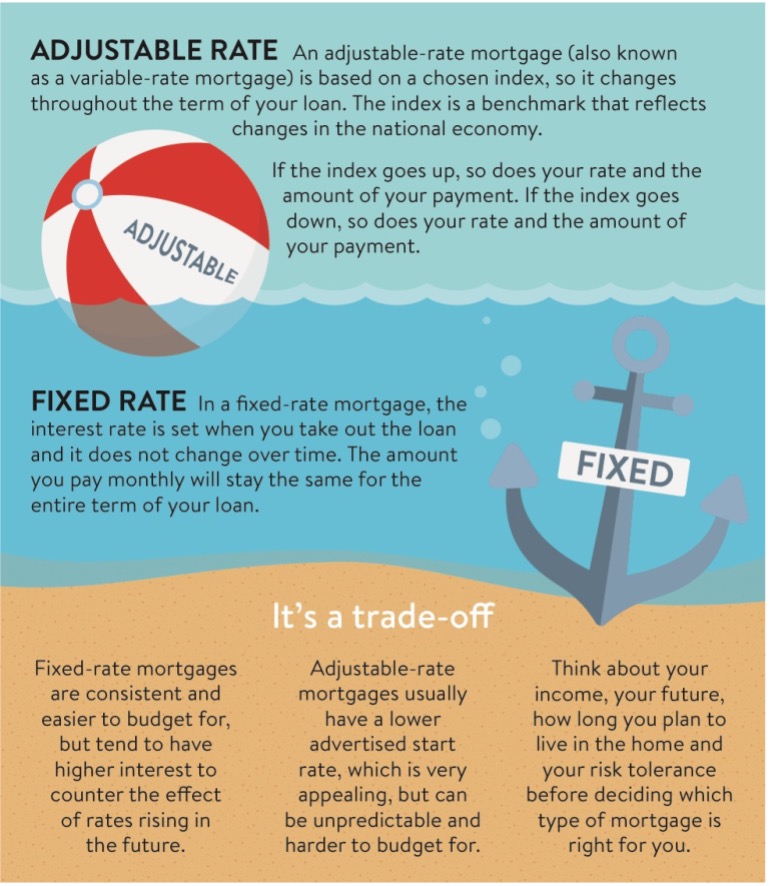

You’ll need to select a fixed-rate or variable rate. A fixed-rate is when the interest rate is set and does not change over time. The amount you pay monthly will stay the same the entire term of your loan. A fixed-rate mortgage can be a bit of a gamble, as rates may decrease, but it does provide cost certainty and making it easier to budget. However, fixed rates tend to be slightly higher to counter the effect of rates rising in the future.

A variable rate mortgage sees the interest rate change throughout the term of your mortgage – sometimes for the good and sometimes for the bad. Financial institutions base the rate change on an index, which usually reflective of changes in the national economy or the rate of inflation. If that index increases, so does your rate and the amount of your payment. If the index goes down, so does your rate and the amount of your payment. Therefore, a variable rate mortgage is more unpredictable and harder to budget for than a fixed-rate mortgage.

Consider your income, your future, how long you plan to live in your home and your risk tolerance before deciding which type of mortgage is right for you.

No matter which mortgage you select, you can make your payments monthly, bi-weekly or weekly, whatever suits your life and your budget.

Amortization is the total length of time it’ll take you to pay off a mortgage, usually in years. The amortization schedule will show you how much of each payment is going towards interest and principal. The payment is the amount paid by the borrower during each set period (monthly, biweekly, etc.) that ensures that the loan is paid off in full with interest at the end of its term. A big chunk of your monthly payments go towards interest at the start of the term. Over time, more of your payment will go towards the principal than towards interest.

During your amortization, you’ll be able to renew your mortgage, which provides an opportunity for you to renegotiate the terms, including the rate. You can usually choose how long you wish to wait before renewal, generally between six months and five years. Generally speaking, shortening the time between renewals will likely mean a higher interest rate. If you negotiate a renewal before your chosen time is over, you may be subject to a financial penalty.

A mortgage can be an empowering experience or a burden. It all comes down to your understanding of mortgage products available, honesty regarding your finances and clarity about your life situation.

People get in trouble by committing to a mortgage they don’t fully understand. All the more reason to know what you’re getting into before signing anything.